While the investor rush into passive strategies benefited fund behemoths, some active funds are innovating to win inflows against the tide.

While passive strategies continue their dominance in traditional market segments, the industry’s evolution suggests a more nuanced future, based on Global Trading analysis of 1,100 funds tracked by Morningstar. Active managers are carving out new investment spaces in complex strategies where expertise and risk management capabilities attract flows.

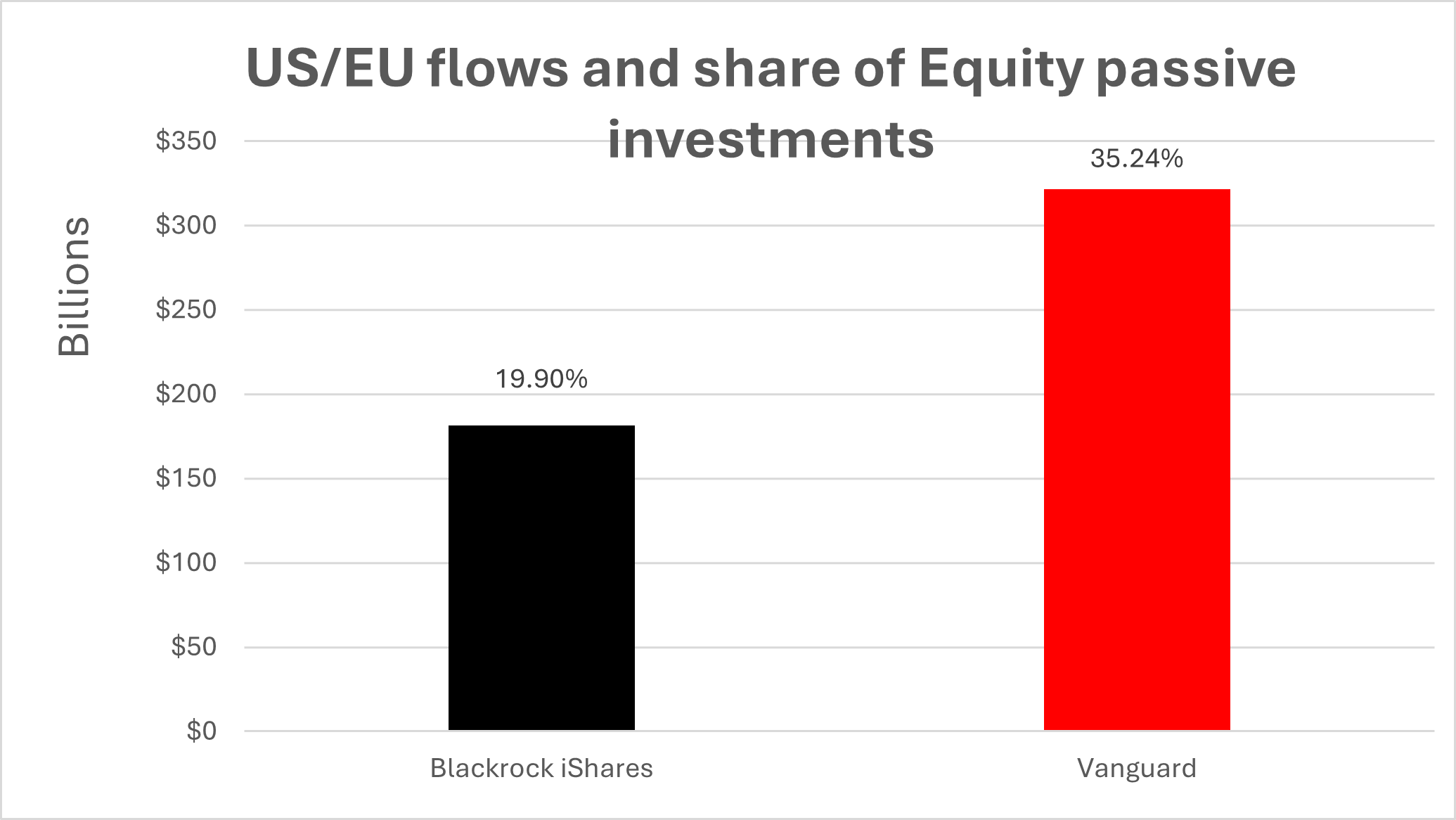

In the passive investing space, Vanguard and Blackrock use scale to dominate, seeing inflows of more than US$73 billion in Europe and US$433 billion in the US, while their actively managed counterparts suffered outflows of US$297 billion, according to Morningstar data.

The shift has been particularly pronounced in the US, where passive exchange-traded funds (ETF) have become “the default investment choice,” according to Morningstar analyst Jose Garcia Zarate. The 4 largest exchange-traded funds (ETFs) tracking large-cap US stocks include funds managed by Blackrock and Vanguard with a total US$4.34 trillion in assets passively tracking the market. In the US, Vanguard passive equity vehicles saw inflows of US$305.3 billion during 2024.

Innovation and idiosyncrasies drive rarer positive flows for active equity managers

However, the picture is not unremittingly gloomy for active funds, particularly for those who can repackage their stock-picking skill in lower-cost packages that attract fee-conscious investors.

Product innovation remains concentrated in the ETF segment, with active ETFs representing 2.5 per cent of EU ETF assets and 8.5 per cent of US assets according to Morningstar. However, these vehicles differ markedly from traditional active funds, maintaining lower tracking errors and expense ratios to compete in an increasingly cost-conscious market. Complex alternative strategies have emerged as one of the few segments of active management gathering funds, particularly in derivative-based products. JPMorgan’s Equity Premium Income ETF, the category leader with US$ 36.9 billion in assets, exemplifies this trend. Together with its sister fund, the Nasdaq Equity Premium Income ETF (US$ 20.7 billion), JPMorgan dominates the derivative income space, which has attracted US$29.36 billion in fresh capital this year while the category delivered returns of 17.68 per cent.

In the Defined Outcome segment, Innovator ETFs and First Trust advisors have established themselves as the premier providers, at year-end they managed approximately US$ 9.37 billion in assets.

In Europe Pictet hemorrhages while Capital Group gains ground

The European equity management landscape presents a more nuanced picture. While passive strategies dominated with inflows of US$263.2 billion, active managers demonstrated resilience in specific segments despite seeing US$62.6 billion in outflows. Total net flows into European funds reached US$169.3 billion year-to-date, marking a substantial recovery from 2022’s outflows of US$19 billion.

Those that used mega-cap dominated benchmarks or followed strongly performing emerging markets, did best. Active managers attracting European investors included Capital Group which gained more than US$ 3 billion of inflows in its Perspective funds whose largest holdings include Meta Platforms and Microsoft. Meanwhile, Austria’s Union Investment and Germany’s Deka gained both about US$2 billion of flows into their family of funds. Goldmans Sachs Asset Management had a great year with more than $US 2 billion of inflows in their European vehicles focused on India, Japan and China. This contrasts with Swiss group Pictet, whose equity funds bled more than US$ 9.3 billion during 2024, according to Morningstar. Including fixed income, Pictet’s fund flows were overall positive in 2024, a spokesperson for the company said.

ESG loses lustre

Perhaps the most notable shift in European equity markets has been unprecedented outflows from environmental, sustainability and governance (ESG)-focused active funds. European ESG-driven funds led by BlackRock’s Climate Transition Screened World Equity Fund (AUM US$16.9bn), have experienced the region’s largest outflows at US$15.5 billion in 2024, according to Morningstar. Notable losers in this category are Nordea (US$2 billion), Pictet (US$1.2 billion) and Schröders (US$1.02 billion).

Alternative energy funds have faced similar headwinds, with active strategies in this space seeing US$8.3 billion in outflows from a US$29.3 billion asset base. “In Europe, there is an ongoing deceleration for sustainable investment products,” noted Morningstar’s analyst Jose Garcia Zarate, highlighting a trend that has become increasingly apparent over the past two years.

©Markets Media Europe 2024