Traditional firms backing EDX Markets and applying for spot bitcoin ETFs mark a turning point.

The second quarter of 2023 may be remembered as the moment the establishment commenced its veritable land grab for crypto according to a report from Genesis, an institutional digital assets financial services firm.

Genesis said in its Q2 Market Observations report that at the mid-point of 2023, the digital asset space has taken on a decidedly transitional feel awaiting the next watershed moment.

“Just as crypto mainstays like Coinbase rolled out new offerings, Q2 also heralded the arrival of an establishment armada which appears now to be docked on the shores of this asset class,” added Genesis. “We view this development as the omen of a bright future that foreshadows a restoration of access, a proliferation of fresh products/services, and an unblocking of legal logjams.”

The trading desk at Genesis observed an increase in client activity across segments which it said was bolstered by promising developments such as the favorable Ripple ruling, the launch of offshore futures by Coinbase, and the emergence of EDX Markets, the spot crypto trading platform backed by Citadel, Fidelity and Schwab and which has partnered with Talos, which provides institutional trading technology for digital assets.

In July EDX Markets said in a statement it has integrated with Talos’ end-to-end order and execution management system (OEMS). By integrating with Talos, EDX Markets gains access to a network of more than 40 liquidity providers including exchanges, custodians, OTC desks and market makers.

Jamil Nazarali, EDX Markets

Jamil Nazarali, EDX Markets

Jamil Nazarali, chief executive of EDX Markets, said in a statement: “This collaboration broadens our range of liquidity options for clients, reinforcing our commitment to delivering a comprehensive and robust trading experience for both traditional financial institutions and crypto-native firms.”

Anton Katz, co-founder and chief executive of Talos, told Markets Media that EDX Markets is backed by institutional players, very similar to Talos’ backers and there is some overlap between their customers.

“We were in touch with the EDX team pretty early on and we also had client demand from our side to connect,” Katz added. “EDX definitely sends a signal that the market is becoming more regulated and institutionalised, which was one of our bigger bets.”

Katz continued that crypto is moving towards a more sophisticated, more regulated and more institutional market which is a step in the right direction. For example, the EDX offering is very familiar to institutional players by letting them match trades with other institutions with whom they have a counterparty relationship.

Genesis said: “The preeminence of counterparty consideration foreshadows the next wave of institutional crypto adoption, which may include more advanced iterations of prime services offerings and execution and operational facilities, both on- and off-chain.”

As more institutions enter the crypto market, they increasingly expect the same tools as they use in other asset classes. As a result, in July Talos launched a new post-trade analytics interface on its trading platform in which users can visualize their historical trading data through a set of interactive dashboards, including by market, symbol or transaction cost analysis (TCA) by strategy.

Talos intends to roll out advanced post-trade analytics, which will include real-time, algo-level and order-level performance (e.g., slippage, markouts, volume participation, maker rate).

Anton Katz, Talos

Anton Katz, Talos

“We built our own transaction cost analysis tools to make sure we have a full understanding of how our execution layer works and bring complete transparency,” said Katz. “The tool allows clients to analyse our algorithms which I believe are the most advanced in the market for execution. We say don’t trust us – trust the data.”

Institutions also use pre-trade data as a guide for how to approach the market and Katz said Talos will make announcements on providing pre-trade data when the firm is ready.

He highlighted that, in comparison to traditional capital markets, digital assets have data that is transparent at the blockchain level.

“Providing data in a more real-time, more transparent way is where crypto and digital assets will shine because of the underlying technology,” Katz added. “If reporting becomes more real-time, then trading can become more capital efficient.”

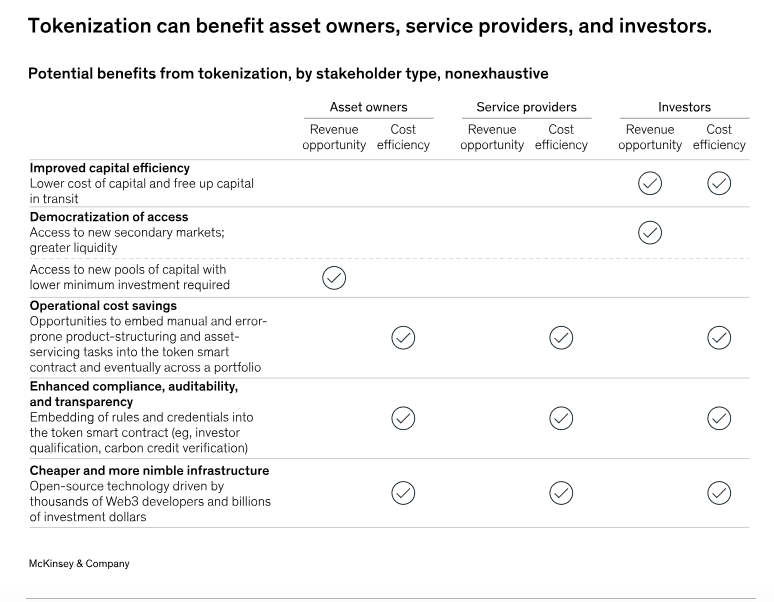

Source: McKinsey

Source: McKinsey

ETFs

Genesis said in its report that block trade volumes, a proxy for institutional grade activity, have been rising relatively unabated for some time.

“The prospective ability to express views on crypto majors through one or more spot-based ETFs managed by household TradFi names like BlackRock and Fidelity alongside a spot-trading venue (EDX) supported by them (and their peers) is likely,” added Genesis.

The US Securities and Exchange Commission has not approved any applications for spot bitcoin ETFs, although the regulator has approved ETFs on listed bitcoin futures.

On July 19 2023 five bitcoin ETF applications from BlackRock, Fidelity, Invesco Galaxy, VanEck and WisdomTree were published in the Federal Register, which sets a timeline for the SEC to review the proposals

Genesis said the introduction of ETFs in the past has proven a meaningful catalyst for further price appreciation in the underlying asset.

“Such was the case for assets previously considered ‘fringe,’ from junk bonds to emerging market debt and precious metals, which now form a core part of most macro portfolios, for which index and ETF access product is now rife and which experienced a material appreciation post-ETF launch,” added Genesis.

David Howson, Cboe Global Markets

David Howson, Cboe Global Markets

David Howson, global president of Cboe Global Markets, said on the group’s second quarter results call that the exchange has applied for regulatory approval of spot Bitcoin ETFs on behalf of five issuers and has surveillance sharing agreements in place with a number of crypto trading platforms. He said that if they get approved it will be positive for the industry and for investors who want regulated exposure to crypto.

“The market makers involved in those ETFs and the create and redeem process are going to need to hedge that potential exposure,” Howson added. “They’ll look to a spot and futures market in order to do that.”

Genesis continued that a robust crypto derivatives market could also usher in institutional adoption on a global scale. For example, the crypto options market volume for the first half of this year was only 10% of underlying spot volume.

“As a corollary, the notional volume of equity options in the US exceeded the notional traded value of the underlying equities in 2021 for the first time,” added Genesis “If following this TradFi trend, the crypto options market has room to grow 10-fold from current levels.”